Gretlin Prukk explains how Assistants can shine during the startup fundraising process

If you are working in a startup, you have definitely heard of fundraising. If you are new to the game and need to get up to speed fast, here are some insights that might be helpful.

What Is Fundraising?

Every company needs money to run the business, and a startup is no different. One option for acquiring capital is to raise money from investors. There are different funding rounds and types of investors depending on the stage of the startup.

Fundraising is a company-wide project led by the CEO with the support of an experienced CFO and management team. Depending on the round, this process might take from three to nine months. As an Executive Assistant in a high-growth startup, I’ve had the opportunity to get the closest look possible into two fundraising rounds.

The latest of the two was the Series B round that resulted in the highest Series B raise to date in the IDV (identity verification) market, with two top-tier venture capital firms joining the team. The whole fundraising process took place during the pandemic, which meant we had no physical meetings with the investors; everything was done virtually.

I will be sharing some personal insights and practical tips, so when you are looking for information on how to support your executive before, during, and after the fundraising process – I hope this article helps you along the way!

The Fundraising Process

Before

My current company was my first startup, so the learning curve has been steep. I have been supporting the Founder and CEO of the company and he has been leading the fundraising rounds. So, from the very beginning, I knew I would be very closely included in every detail of the process.

As with any project, I started off with getting an understanding of the whole fundraising process. The beginning of the process is a bit messy, and the road is not yet defined.

As Assistants, we must be inherently adept at project management. This is your chance to shine! Ask a lot of questions, push for clearly defined plans and deadlines, and make sure that you leave every meeting with all action items having an owner and a deadline. You can help your team by identifying the scope of the whole process as you stand outside of all departments and maintain the big picture. The Assistant acts as an invisible glue which brings all details seamlessly together.

I organized short meetings with internal stakeholders to match expectations and keep everyone on the same page on deliverables: I circulated a checklist for the relevant documents for the due diligence process (due diligence is the last step of the fundraising process, where the legal teams check the records of the company before finalizing documents are signed and the money transferred), sent calendar reminders for deadlines and highlighted possible roadblocks (e.g.,“it will take X days to assemble the pitch decks into a visually and contextually coherent unit”).

I made sure that we tested the calendar invite and video call settings, optimized and set up the room for making calls (screens, cables, angles, background, lighting, etc.). We tested the pitch numerous times to take the edge off when presenting and to raise confidence.

From the very beginning, I tried to keep the documentation as simple as possible. Our sources of truth were the main spreadsheet and the investor database.

Main spreadsheet

I started by creating one all-encompassing spreadsheet, collecting every piece of information about the project and its scope. As the owner of the document, I could ensure that this was the single source of truth for the project.

This spreadsheet included the following tabs:

1. Timeline with milestone deadlines and color-coded status.

2. Process divided into action items with owners and deadlines.

3. Checklist of due diligence topics to be cleared and documents to be collected.

When we had our first preparatory meetings, this spreadsheet did not have a clear structure, nor did it have all the information. But it evolved during the process and remained in use until the end. It was the main document to give answers at every meeting when someone asked, “Where are we at? What’s next?”

Investor database

As a second source of information, I created a spreadsheet with all the information about the investors. As the investor list grows longer, it is of utmost importance to be able to know everything at a glance.

I set up a categorizing system to help us focus: Tier1 [M1] investors; investors with more preferable terms; investors with whom we had already had contact; investors who had conflicts through other investments. I also added every single piece of relevant information that I had: contact information, time zone, status (e.g., “Intro needed,” “Catch-up call needed,” “Waiting for reply,” etc.), last and next date of contact, Non-Disclosure Agreement (NDA) status, shared documents, and next steps.

This process is a lot easier when there is already an investor relations system in place. If you have to start from zero, talk to your CEO, go through emails and previous materials for any clues, and do your research on the internet.

As the process moves along, there might be close to 100 investors in your contact list; therefore, a very detailed and always up-to-date database helps you not to drop any balls.

Pitch deck(s)

The core of the fundraising process are the pitch meetings where the CEO meets potential investors and presents the company. The accompanying presentation, called the pitch deck, contains key information about the company, the product and/or services, key metrics, and the business plan. In our case, we invited a professional designer to help us put together the main deck. Different departments also created a couple of additional deep-dive decks (e.g., product and tech, strategy and growth).

I remained the owner and overseer of all the decks and edited them to have the same visual look and style. Pitch decks are circulated to the largest external audience, so they must look professional and coherent, reflecting the company’s brand. Assembling and perfecting your presentations is a bottomless hole and it is easy to spend days of work on them; however, at some point you just must decide that this is now good enough and stop.

During the fundraising process, I updated relevant graphs and metrics, and iterated based on feedback. When a change was introduced on one of the pages, I had to make sure that it was reflected in all the decks (approx. 120 pages). To make that possible, try to keep only one version of every deck. If even two almost-identical versions circulate, you will soon lose track of changes.

Virtual data room

At some point, you must share confidential materials with external stakeholders. For security reasons, email attachments and Google Doc links are a definite no-go. Luckily, there is a nifty solution called a “virtual data room” and it’s meant exactly for this kind of process.

A virtual data room is a secure space for storing and sharing of all relevant confidential materials regarding the fundraising and the due diligence process. A good data room has features like advanced and granular permissions, notifications, Q&A tool, NDA signing, adjustable structure, watermarking, reports, audit trails, multiple-factor authentication, etc.

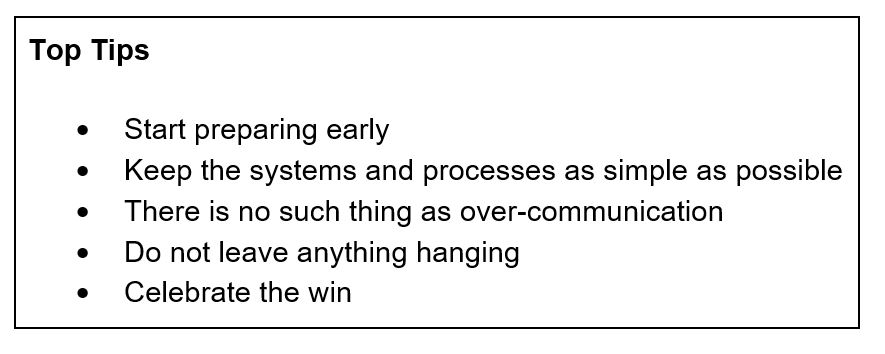

Start as early as possible to look for the best solution matching your needs. Testing security features and Q&A, as well as setting up folder structures and user access, takes longer than you might think. Do not cut corners on testing – if something (technical) can go wrong during the process, it definitely will, and that can be a very costly business-sensitive mistake!

During

Investor calls

The bulk of the fundraising process is taken up by time for the CEO to attend investor calls. I was the point of contact (POC) for all potential investors, so during this time my main tools were my inbox and the CEO’s calendar. My rule was to reply to any incoming email within one hour during our set working hours, taking into account that we were dealing with investors from different time zones across the globe.

One piece of advice is never to set up the first call with your top choice investors. The first pitch is never the best; leave a couple of meetings for practice runs and to collect feedback on your pitch.

After every investor call, collect the CEO’s feedback and next steps and add these to the investor database. Make sure that all action items will be followed up. At one point in the process, there will be just too many meetings to schedule and not enough hours in the CEO’s calendar. This is the point at which the investor database comes in handy. You have the investors categorized by their time zones, their status, and place in the process funnel, in addition to all relevant comments. This helps you to decide which calls to schedule first and which can be stalled a bit if needed.

At one point my executive ran late, and I had to jump on an investor call. Therefore, it is essential that you do your homework on the investor and provide the executive with a memo about the firm and the people they are meeting. And if you have to take over the call, you are ready to be the face of the company for that call.

Deep-dive calls with the management team

After a couple of calls between the potential investor and the CEO, they want to get to know the rest of the management team. This means that each of the management team members will have separate calls with the investors for deep-dive topics. It is important to give fair warning to the team that they need to be ready to find time in their schedule. You can then help by being the POC between the investor and your management team when setting up the calls.

Keeping up with communication

During fundraising, one of the things that may be forgotten is the importance of constant and effective communication between stakeholders. Every involved person, team, and department needs updates to stay on the same page, to support, and to plan their schedule. Keep track of the to-do items and deadlines and push the team to delivery. We used a mix of daily calls with the core team, weekly calls with the board members, and weekly written updates for the management team. We also had a separate Slack channel for the core team, where we kept an ongoing list of action items, questions, and feedback.

After

Once your team has made it to the term sheet, due diligence and transferral of the money, your work is not yet done. Every successful project needs a good closure. Wrap up the project by sending the investors who did not join the round a friendly yet professional individual email. Also, thank every external service provider (e.g., legal, PR, design). Help the CEO to communicate the fundraising results to the whole company: give an overview of results, introduce new investors and board members, and do not forget to leave room for Q&A.

Organize a project retrospective meeting with the management team. Do not forget feedback from investors – it is smart to include this in the investor database for any future needs.

Welcome the new investors and board members to the family. Bring them together with current investors and board members via email or over a dinner. Do not forget welcoming gifts and company merchandise.

By this time, you are probably really tired and dreaming of a holiday! There is just one last thing, and this is to celebrate. You have done an amazing job!